What were the headline numbers for Latin America in 2025?

What were the headline numbers for Latin America in 2025?

The 2025 vintage reveals a decisive decoupling between activity and capital deployment. While transaction volume remained statistically stagnant—contracting slightly by 1% to 2,826 deals—aggregate deal value surged by 31% to reach USD 114.8bn.

This figure represents the highest valuation peak of the last four-year cycle, significantly outperforming even 2022 levels despite a lower transaction count. The data confirms a flight to quality: investors have shifted away from high-volume mid-market consolidation toward high-conviction, large-cap acquisitions, driving the average deal ticket up by 32%. For advisors, the implication is clear: the market has traded frequency for magnitude.

Why This Report Matters?

Why should this report

be on my desk?

Identify new client opportunities.

Identify new client opportunities.

Uncover the specific US and UK corporates actively acquiring in Latin America right now. We highlight the mid-market buyers often missed by global platforms, providing you with a high-probability target list for your next business development initiative.

Benchmark your firm’s LatAm practice against your US/UK peers.

Benchmark your firm’s LatAm practice against your US/UK peers.

Measure your market standing with precision. We rank the international firms winning the most inbound mandates, allowing you to benchmark your deal volume and value directly against your primary competitors in London and New York.

Find top-tier domestic co-counsel for your next inbound mandate.

Find top-tier domestic co-counsel for your next inbound mandate.

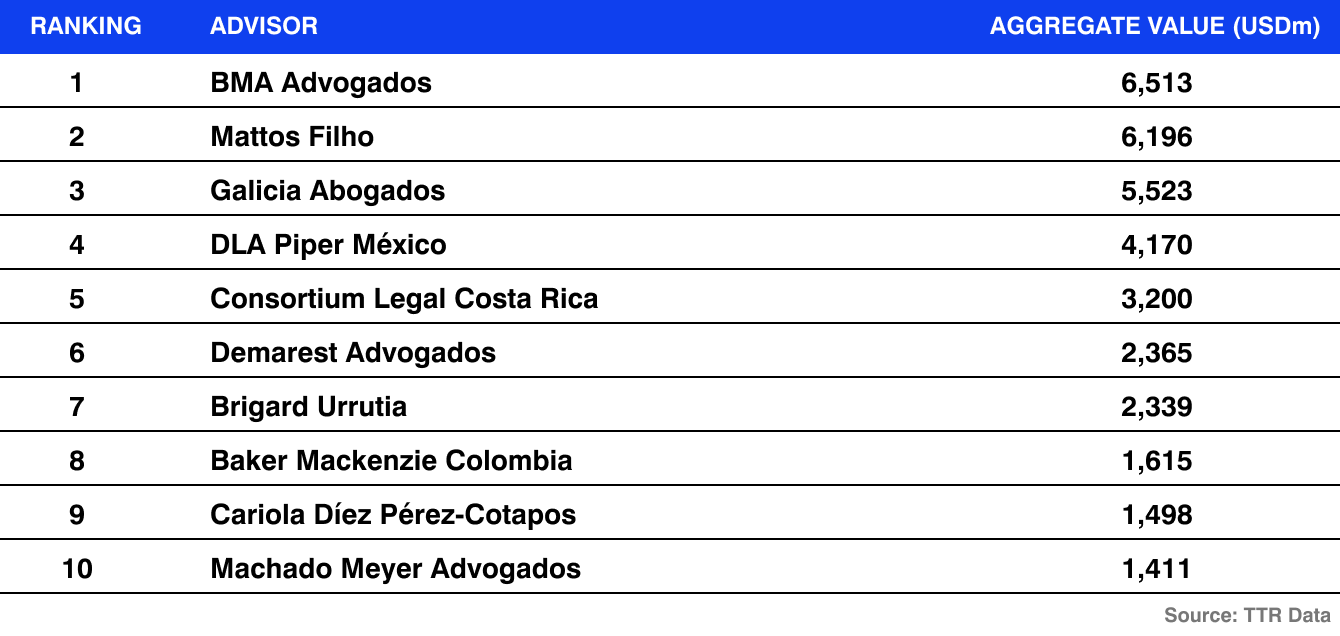

Streamline your partner selection process. Our data reveals the local Latin American firms most frequently retained on inbound deals, offering a validated “shortlist” of top-tier domestic counsel to ensure seamless cross-border execution.

Market Overview – Deal Count & Value

Which LatAm countries were the

most active M&A markets in 2025?

Latin America Market Overview – Sector Breakdown

Which sectors are driving M&A

activity in Latin America?

What’s Driving the Deals?

What are the key trends behind

the numbers in Latin America?

Backbone

The region is witnessing a massive “infrastructure race” driven by the demands of AI and nearshoring. We observed a synchronized rush for physical assets across markets: from BlackRock’s GIP acquiring data centers in Mexico, Brazil, and Chile, to the aggressive consolidation of industrial real estate (FIBRAs) in Mexico and port logistics in Peru. Capital is no longer just chasing software; it is securing the concrete, power, and connectivity required to run the digital economy.

Simplification

The era of the “strategic alliance” is giving way to the “strategic buyout.” Across the region, major controlling groups moved to dissolve long-standing Joint Ventures to regain agility. From Nutresa’s decoupling in Colombia to América Móvil taking full control of ClaroVTR in Chile, the message is clear: in a highvolatility environment, global operators and local tycoons prefer 100% ownership and streamlined decision-making over shared governance.

Security

Energy and food security have decoupled the region’s M&A activity from global ESG hesitation. While Brazil and Chile see continued rotation into renewables, the “hard” commodity markets in Argentina (Vaca Muerta shale) and Peru (Copper/Agro-export) attracted significant US and European capital. Foreign strategics are effectively “locking in” their supply chains, acquiring the raw production capacity for everything from lithium batteries to winter produce.

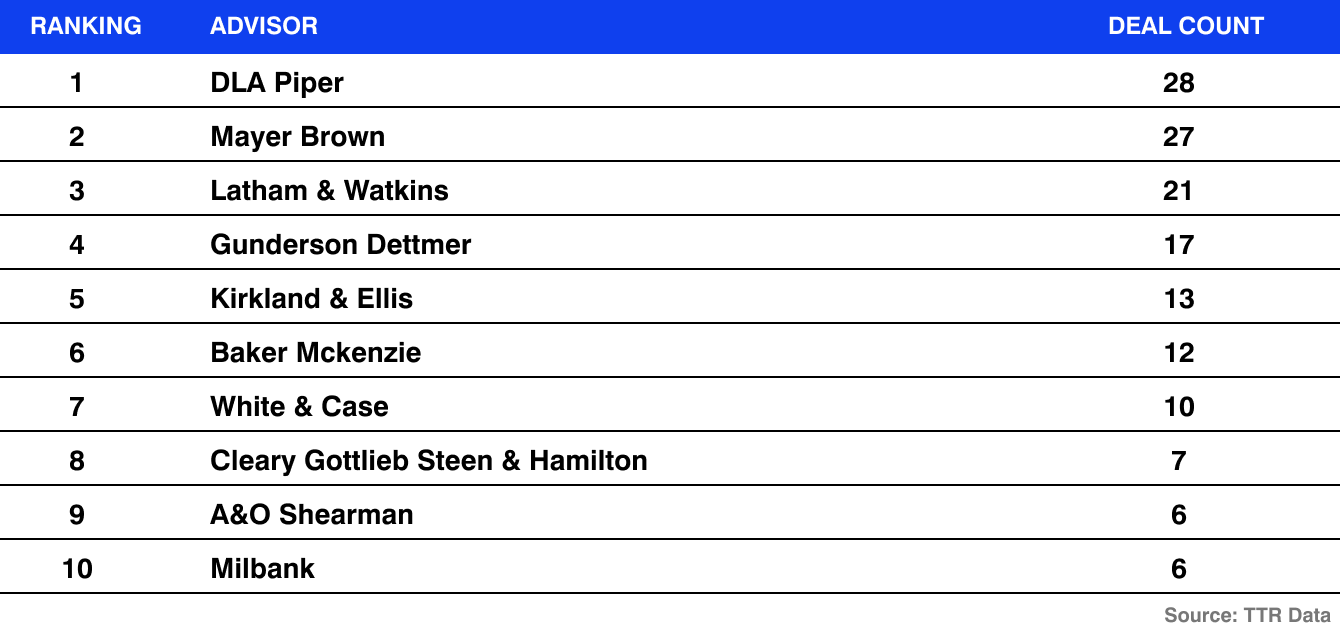

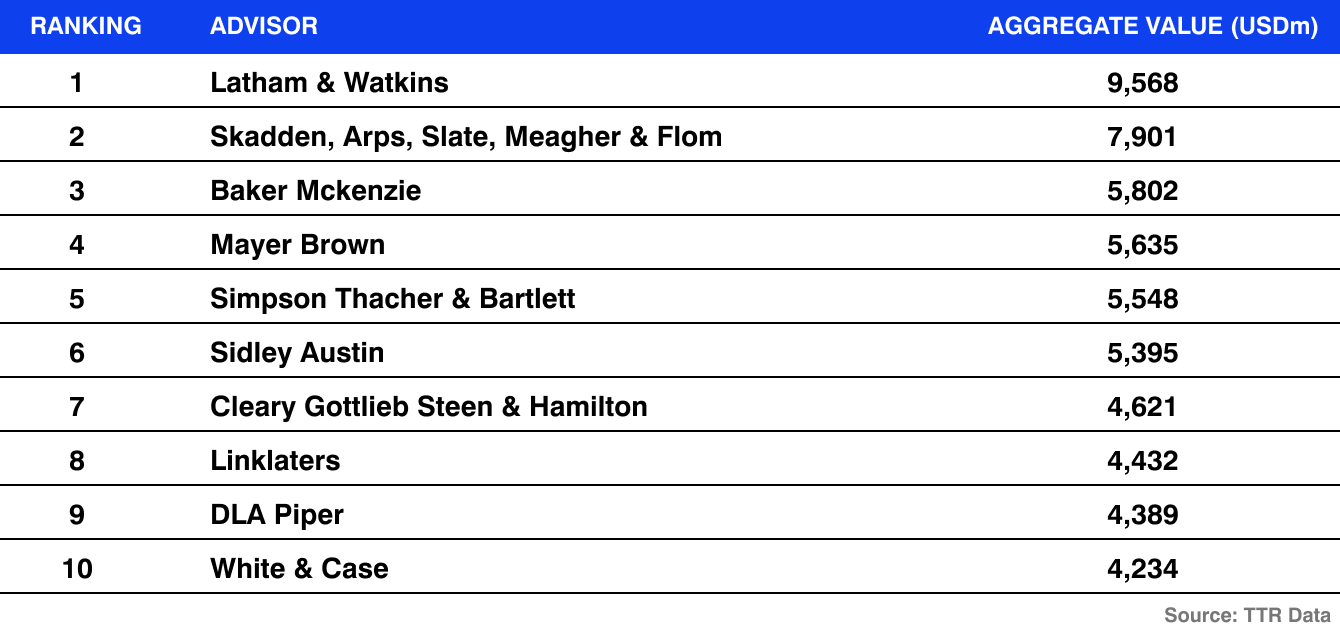

US & UK Global Law Firms: Top Advisors by Deal Volume & Value

Which US & UK firms lead the market in

deal activity and aggregate value, in 2025*?

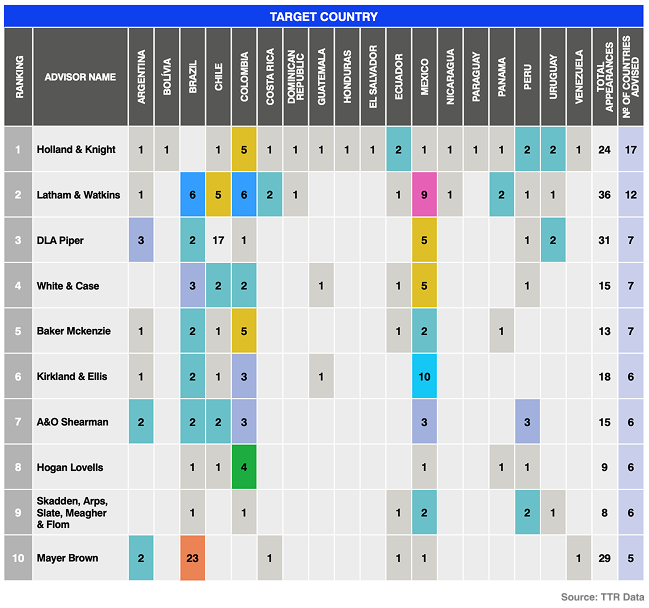

US & UK Law Firm Footprint: Regional Breadth & Coverage

Which US/UK firms possess the deepest

local capabilities across the region*?

Buyer-Origin Ranking 2025

Which foreign countries are

buying Latin American targets?

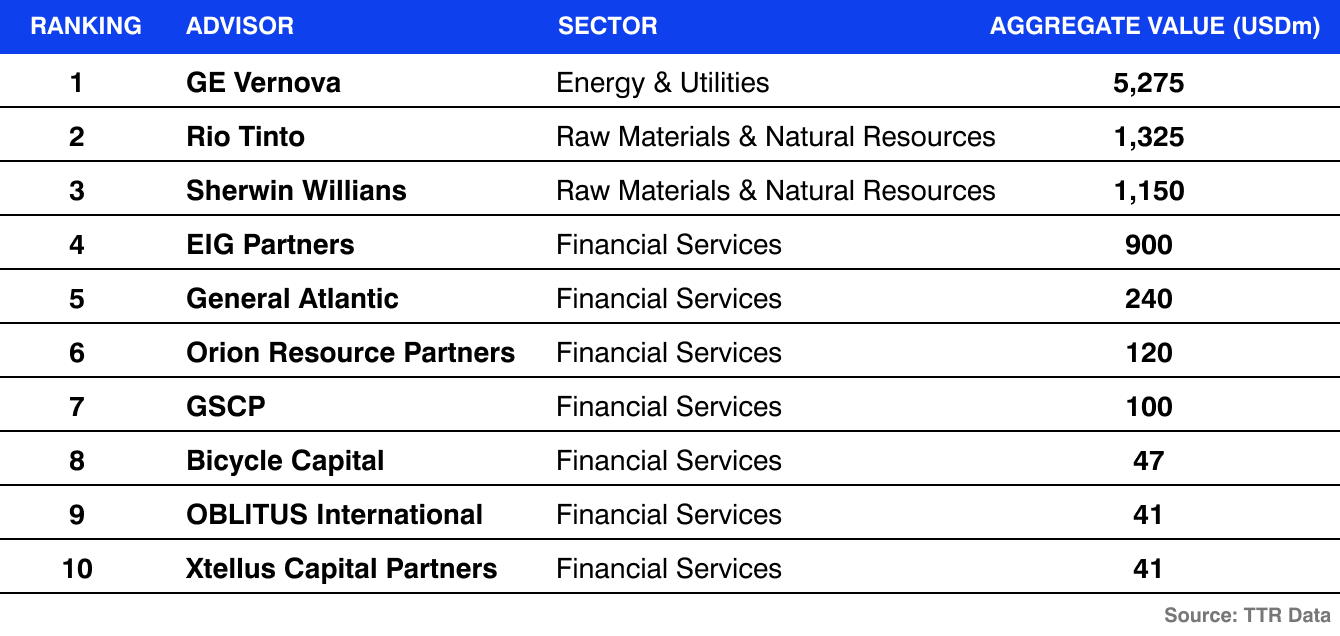

Top 10 US/UK Buyers in LatAm

Which specific US & UK companies were the

most active buyers in Latin America?

What are my US & UK Clients Buying?

Which sectors are US & UK

buyers investing in?

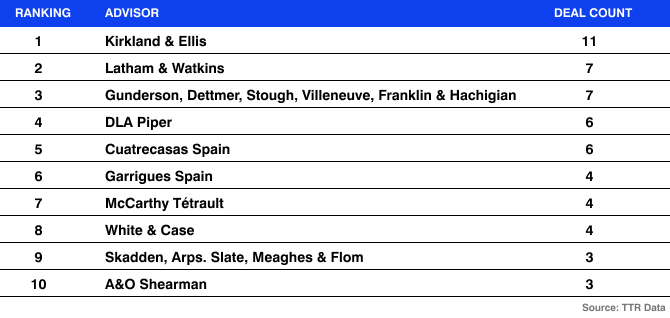

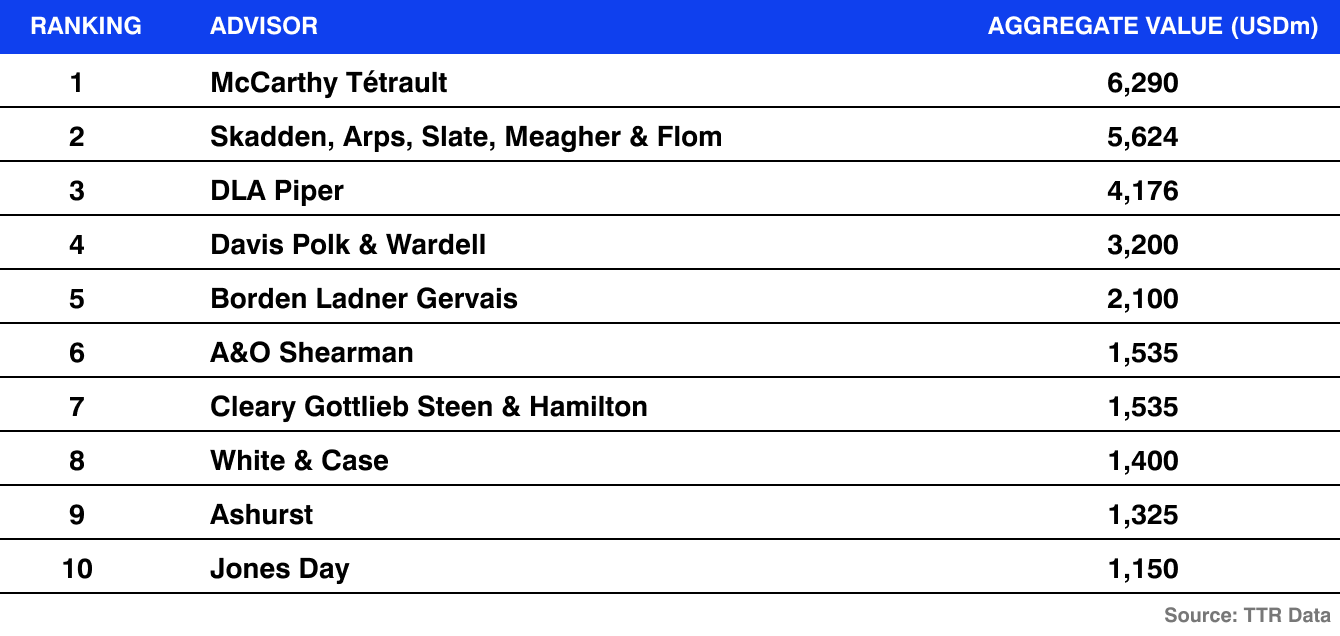

International Legal Advisors: Inbound Buy-Side Rankings

Which international firms are the primary

gateways for foreign investment entering the region*?

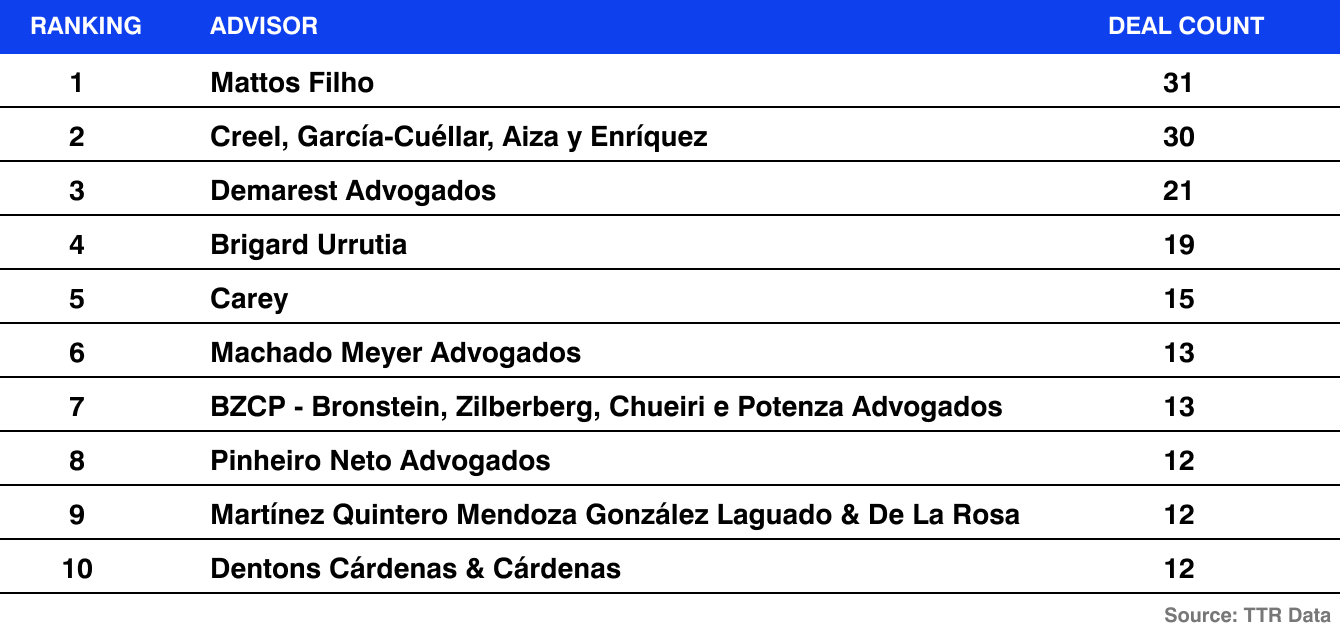

Top Domestic Co-Counsel: The Inbound Shortlist

Which Domestic LatAm firms are

advising on the most inbound deals?

How do the “Big 6” Markets Compare for Inbound Deals?

What do I need to know about

the top LatAm markets?

About TTR Data

What makes

TTR Data different?

Conclusion & Contact

How can I get this data

for my practice?